By Vicki Schmelzer

NEW YORK (MaceNews) – Global investors were increasingly more cautious in their views about growth and inflation in August, according to BofA Global Research’s monthly fund manager survey, released Monday.

A net 41% of those polled this month looked for weaker global growth in the coming 12 months. This compared to a net 31% looking for weakness in July and a net 46% looking for weakness in June. As background, in April, a net 82% looked for weakness, the “most on record” (30-year history).

Inflation concerns rose in August, with a net 18% of portfolio managers looking for higher global inflation in the coming year. This compared to a net 6% looking for higher inflation in July and a net 13% looking for higher inflation in June.

Cash levels held steady at 3.9% in August. In July, when the benchmark broke below the psychological 4.0% mark, this triggered a “sell signal” for the S%P 500. Cash levels held at 4.2% in June.

In the 17 “sell” signals seen since 2011, the median 4-week S&P 500 loss has been 2%, the survey said. The “biggest loss recorded post-sell signal” was 29% and the “best gain” was 3%, the survey noted.

Cash allocation stood at a net 1% underweight, the first underweight since February 2025. Cash allocation was a net 6% overweight in July and a net 16% overweight in June respectively.

In terms of asset allocation, other than an increase in equity holdings, global investors showed more caution than in prior months.

In August, a net 14% of portfolio managers were overweight global equities, versus a net 2% overweight in July and a net 2% underweight in June.

A net 5% of those polled were underweight bonds, compared to a net 4% underweight in July and back at June levels.

Allocation to real estate stood at a net 21% underweight in August, compared to a net 10% underweight in July and a net 12% underweight in June.

Commodity allocation was net neutral this month, versus a net 5% overweight in July and a net 9% overweight in June.

When asked about crypto allocation, a net 82% of fund managers said that they have not yet begun to “structurally allocate to crypto” versus 9% who said that they have.

“The weight average FMS allocation to crypto is 0.3% (3.2% among FMS investors who are allocated to crypto,” the survey noted.

In terms of regional equity allocation this month, U.S and emerging markets were favored over the eurozone, while other regions saw only minor changes.

Allocation to U.S. equities held at a net 16% underweight in August, compared to a net 23% underweight in July and a net 36% underweight in June.

This month, a net 24% of those polled were overweight eurozone stocks, down from a net 41% overweight in July, which was a four-year high, and compared to a net 34% overweight in June.

Allocation to global emerging markets (GEM) rose to a net 37% overweight in August, versus a net 22% overweight in July and a net 28% overweight in June. This is the highest GEM allocation since February 2023, the survey said.

“The US is viewed as the region in which equities are the most overvalued by a record net 91% of FMS investors (up from 87% in July),” the survey said.

Conversely, emerging markets were “viewed as the region in which equities are the most undervalued (net 49% say undervalued, most since Feb’24),” BoA Global added.

This month, allocation to Japanese equities improved to a net 2% underweight versus a net 9% underweight in July, while UK allocation held at a net 2% underweight versus a net 3% underweight in July.

In terms of the three biggest “tail risks” seen by managers, in August these were: “Trade war triggers global recession” (29% of those polled), “Inflation prevents Fed rate cuts” (27%) and “Disorderly rise in bond yields” (20%).

Last month, the biggest “tail risks” were “Trade war triggers global recession” (38% of those polled), “Inflation prevents Fed rate cuts” (20%), “U.S. dollar slumps on capital flight” (14%).

In August, the three “most crowded” trades were seen as “Long Magnificent 7” (45% of those polled), “Short U.S. dollar” (23%), and “Long Gold” (12%)

In July, the three “most crowded” trades were seen as “Short U.S. dollar” (34%), “Long Magnificent 7” (26%) and “Long Gold” (25%)

Note: the term “Magnificent Seven” was coined by Bank of America’s chief investment strategist Michael Hartnett, referring to a basket of the seven major tech stocks: Apple, Microsoft, Amazon, NVIDIA, Alphabet, Tesla and Meta.

This month, BofA Global asked special questions about tariffs, Fed Chair Jerome Powell’s replacement and overall Federal Reserve Policy.

On trade, most managers expected a final U.S. tariff rate of 15% (weighted average response) on “Rest-of World imports”, up from the 14% tariff rate envisioned in July.

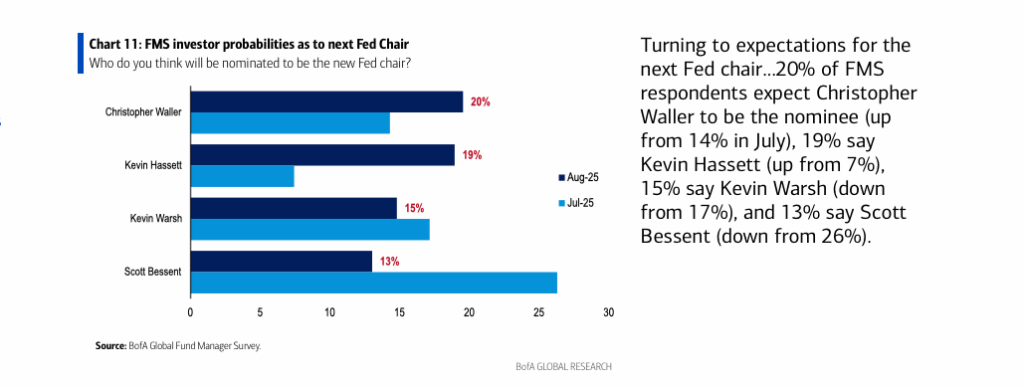

With Fed Chair Powell’s term expiring May 15, 2026, BoA Global polled fund managers about his potential replacement.

In August, 20% of those polled expected Christopher Waller to be the nominee, 19% said Kevin Hassett, 15% said Kevin Warsh and 13% said Scott Bessent.

Last month, the skew was 26% for Scott Bessent, 17% for Kevin Warsh, 14% for Christopher Waller and 7% for Kevin Hassett.

On specific Fed policy, managers were “asked whether the next Fed chair would resort to measures such as QE or YCC to help alleviate the U.S. debt burden” and “54% of FMS respondents said ‘yes’ (36% said ‘no’),” the survey said.

An overall total of 211 panelists, with $504 billion in assets under management, participated in the BofA Global Research fund manager survey, taken July 31 to August 7, 2025. “197 participants with $475bn AUM responded to the Global FMS questions and 99 participants with $183bn AUM responded to the Regional FMS questions,” BofA Global said.

Contact this reporter: vicki@macenews.com

Stories may appear first on the Mace News premium service.

For real-time email delivery contact tony@macenews.com.